Stock/ETF Benchmarker

Stock/ETF Benchmarker

Provides the ability to benchmark a portfolio against a user-selected benchmark index for the current day, and show the contribution and weighting of individual equity positions.

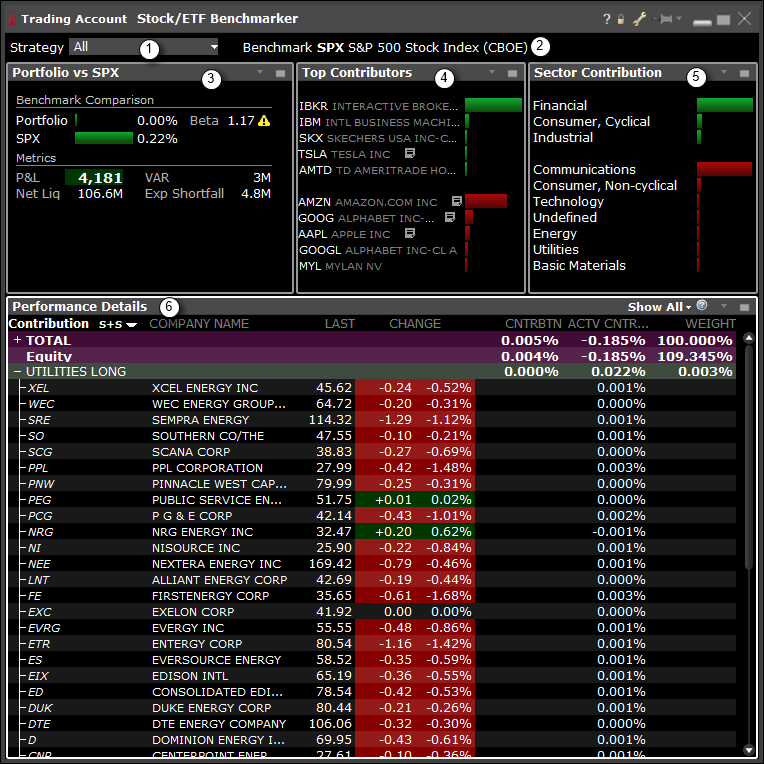

Performance attribution analysis is a process designed to determine how a portfolio is performing relative to a specific benchmark, and to highlight areas of the portfolio that are over- or under-performing. The Stock/ETF Benchmarker displays portfolio performance attribution values which update in real time throughout the day 1.

Open the tool:

- From Mosaic: Use the New window dropdown and from the Technical Analytics section select Stock/ETF Benchmarker.

- From Classic View: Use the Analytical Tools menu and in the Portfolio section select Stock/ETF Benchmarker.

The Interface

- Select a strategy to benchmark.

- Advisors will see individual client accounts plus Model Portfolios, Portfolio Strategies, and account groups.

- The SPX index is used as the benchmark.

- Benchmark Comparison shows your portfolio¹s performance compared to the SPX index. Metrics are the taken from the Account Information window (Net Liq) and Risk Nav (Beta, VAR, Est Shortfall).

- Top Contributors — Sorts contribution to the overall portfolio by security. Lists the top five and bottom five equity components by contribution, indicated both by percentage and graphically using a colored bar.

- Value is also reflected in the Performance Details "Contribution" field.

- Sector Contribution — Sorts contribution by sector. Lists sectors by contribution, from highest to lowest. Indicated both by percentage and graphically using a colored bar.

- Value is also reflected in the Performance Details "Contribution" field.

- Performance Details

- Sorting Entries: Sort by "Sector + Side" or "Industry + Side" (NOTE: more sort selections coming soon).

- Contribution field: Shows the contribution (by percent) of each security or category (ie. Industry) to the overall portfolio.

- Active Contribution field: The difference between the contribution to the portfolio return and the contribution to the benchmark return for a specific security or category.

- Weight field: The weight of each security or category contribution to the portfolio.

- NOTE: Use the "insert" feature to add Benchmarker fields. Benchmark Contribution and Benchmark Weight which show the percent contribution and weight of the security to the overall benchmark.